This blog post presents results of a nationwide survey on the recording of publication costs at research performing institutions in Germany, which was conducted within the framework of the project OA Datenpraxis (OA Data Practice).

In the course of the open access transformation, research performing institutions are spending their funds not only on providing access to scholarly literature but also on publication costs, for example article processing charges (APCs). These costs may be incurred and settled in a very distributed manner within an institution, which makes it difficult to reliably record all information-related expenditure within an institution and hampers the transparent handling of such costs. The fact that the recording of publication costs is a relevant topic for research performing institutions can be seen, for example, in the discourse on the concept of the information budget (Mittermaier, 2022; Pampel, 2019). In this holistic view of an institution’s information-related financial flows, expenditure on publications should be incorporated into budget planning alongside expenditure on subscriptions. In addition, the importance of considering the revenue side, for example publication allowances from funding agencies, is emphasised. In the year 2022, The German Science and Humanities Council (WR) recommended that research performing institutions should establish an information budget by 2025 (WR, 2022). The recording of publication costs may also be mandatory for institutions, for example in the case of funds drawn down within the framework of the German Research Foundation’s (DFG) funding programme “Open Access Publication Funding”.

The DFG-funded project “OA Datenpraxis” examines various aspects of the handling of data in the context of the open access transformation. Besides the recording of publication costs at institutional level, open metadata provisions in transformative agreements, open access in institutional rankings, and open access dashboards, among other things, are analysed.

This blog post presents the results of a survey on the recording of publication costs at research performing institutions and identifies the questions that these results may raise for the open access community.

Procedure

How established is the practice of recording publication costs at research performing institutions in Germany? In the year 2024, representatives of the research project “OA Datenpraxis” at the Berlin School of Library and Information Science at Humboldt-Universität zu Berlin investigated this question with a quantitative survey examining the recording of publication costs at institutional level. It was the first comprehensive quantitative survey on this topic in Germany.

Developing the Questionnaire

The questionnaire was developed based on previous surveys, practice reports, and other preliminary work. It was revised following discussions with staff members from the acquisitions department of a large university library and with representatives of the Projekt DEAL group, with whom a collaboration agreement was concluded. The questionnaire was then pretested with 11 people from 10 institutions. The final version comprised 26 questions.

Creating the Distribution List

The survey was implemented as a personalised online survey. Representatives of research performing institutions in Germany, for example universities, universities of applied sciences, non-university research institutions, and federal departmental research institutions, were included in the distribution list. Of the 583 persons invited to participate, 258 (44.3%) completed the questionnaire. Figure 1 shows the geographic distribution of the invited institutions by institution type.

Monitoring Activities

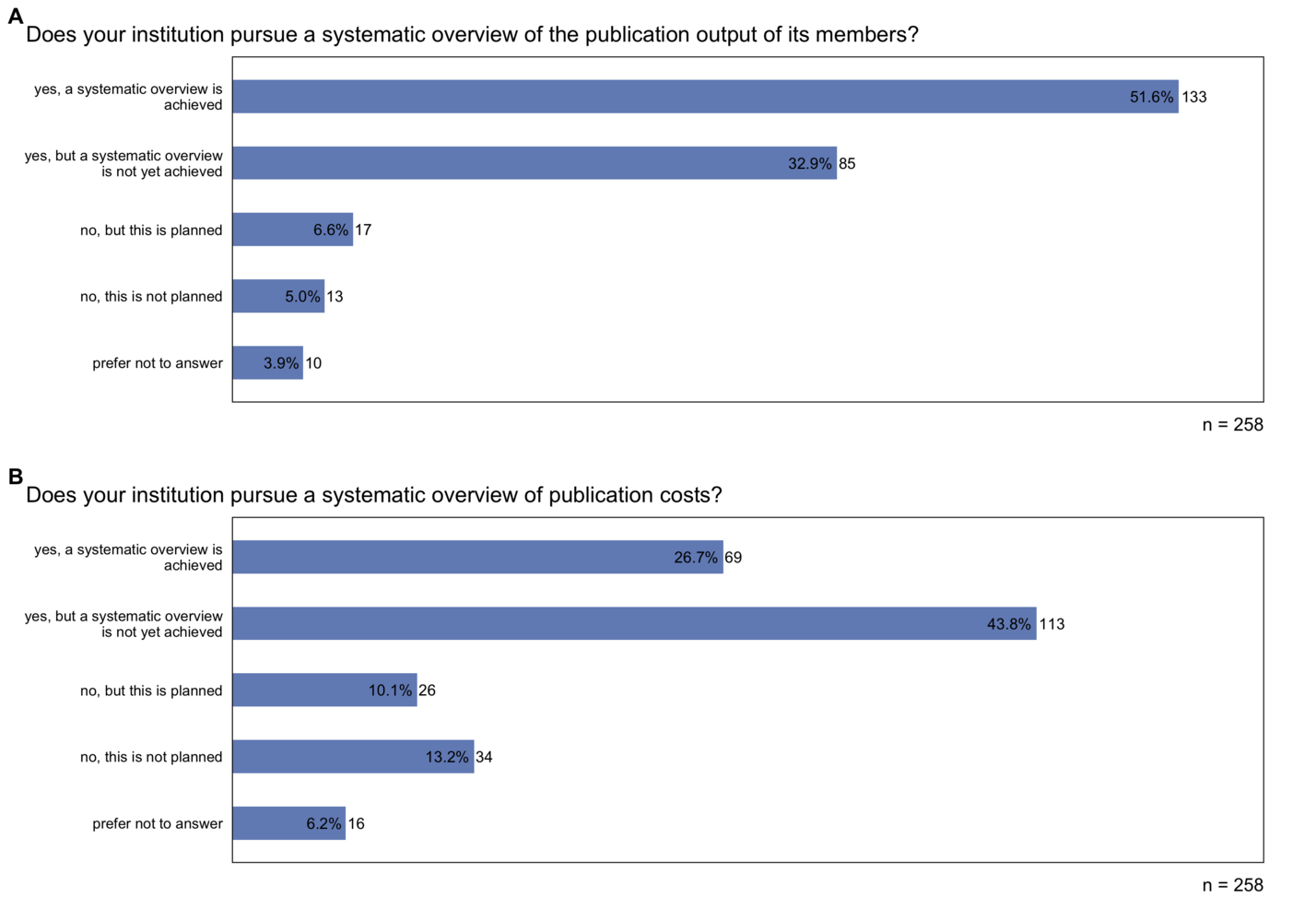

The survey results show that around half (51.8%) of the participating institutions had already achieved a systematic overview of the publication output of their members (see Figure 2A). A further 32.9% reported that their institutions were pursuing this goal.

By comparison, monitoring of publication costs was less widespread, with around a quarter (26.7%) of respondents reporting that publication costs were systematically recorded at their institutions (see Figure 2B). A further 43.8% reported that their institutions were currently pursuing this goal.

Support at Leadership Level

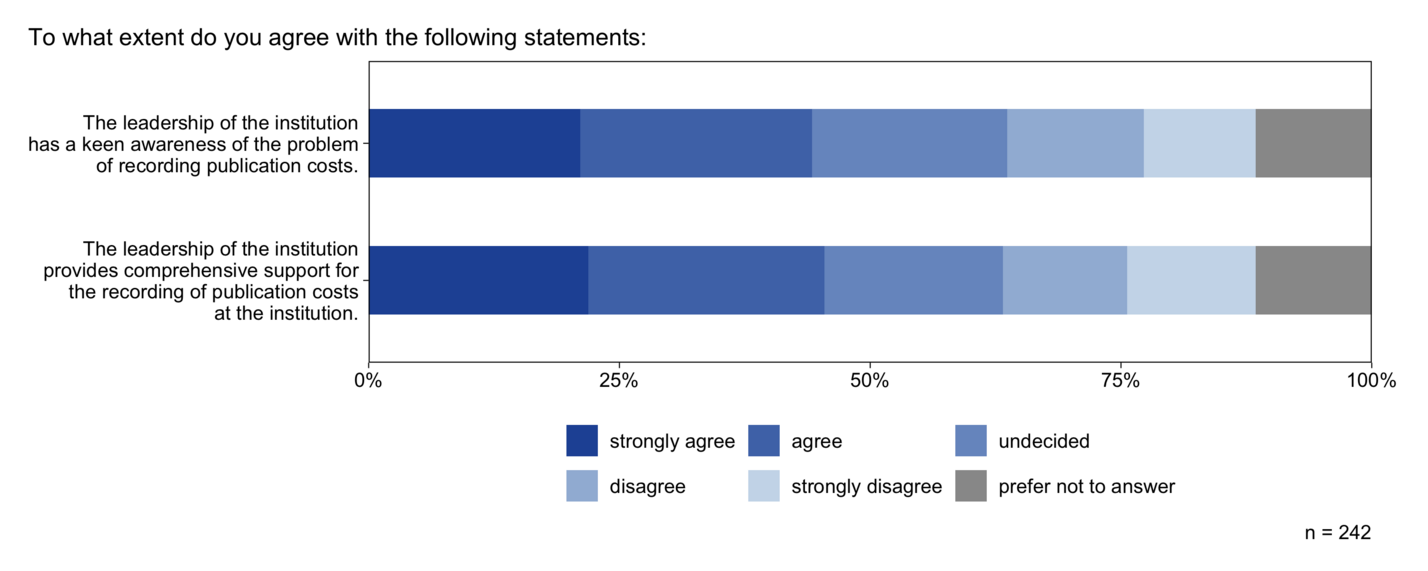

Participants who were not themselves part of the institution’s leadership were asked for their assessment of leadership’s awareness of the problem of recording publication costs and its support for this practice (see Figure 3): 41.5% of respondents reported that they perceived a keen awareness at leadership level of the problem of recording publication costs. This percentage is based on a combination of the response options “strongly agree” and “agree”. A similar percentage of respondents reported that they felt that their institution’s leadership comprehensively supported the recording of publication costs.

Figure 3: Assessment of the institution leadership’s (a) awareness of the problem of recording publication costs and (b) support for the recording of publication costs.

Processes

Some 42.7% of the respondents reported that there were binding processes for the recording of publication costs at their institution. A slightly smaller percentage of respondents reported that processes were in place but were not binding.

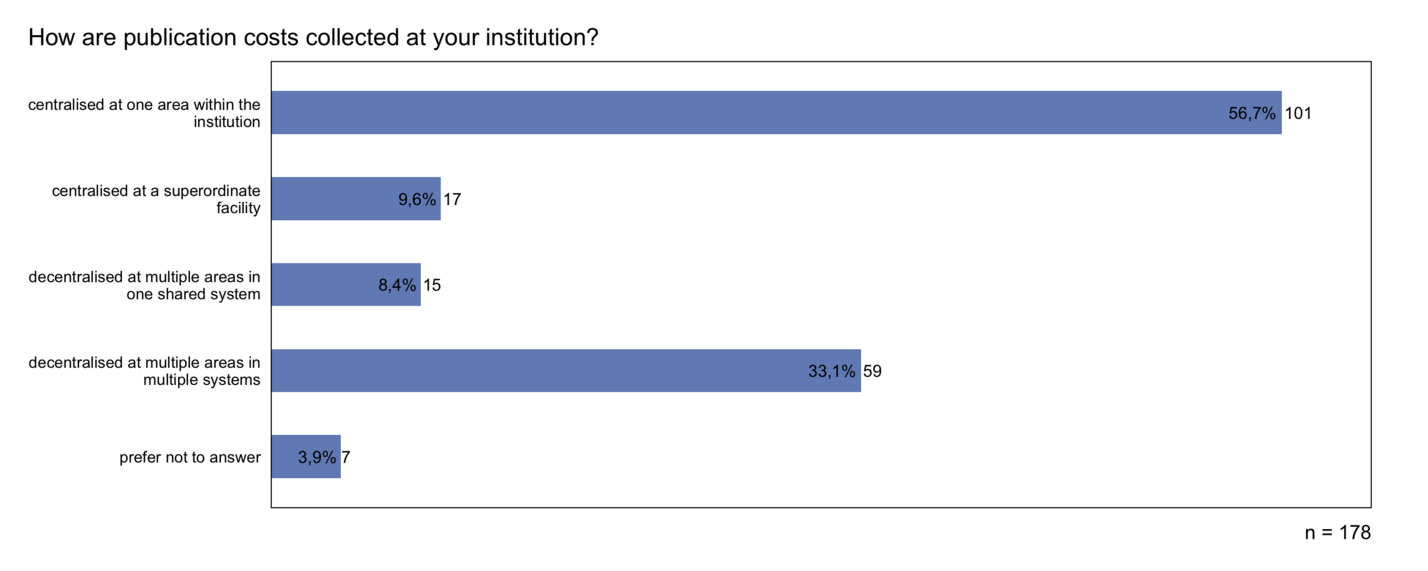

Just over half of the respondents (56.7%) reported that publication costs were recorded centrally in one department at the institution (see Figure 4). In addition, 9.6% reported that recording took place centrally at a superordinate institution. About one third of respondents (33.1%) reported that publication costs were recorded decentrally in several departments or in several systems (Figure 4).

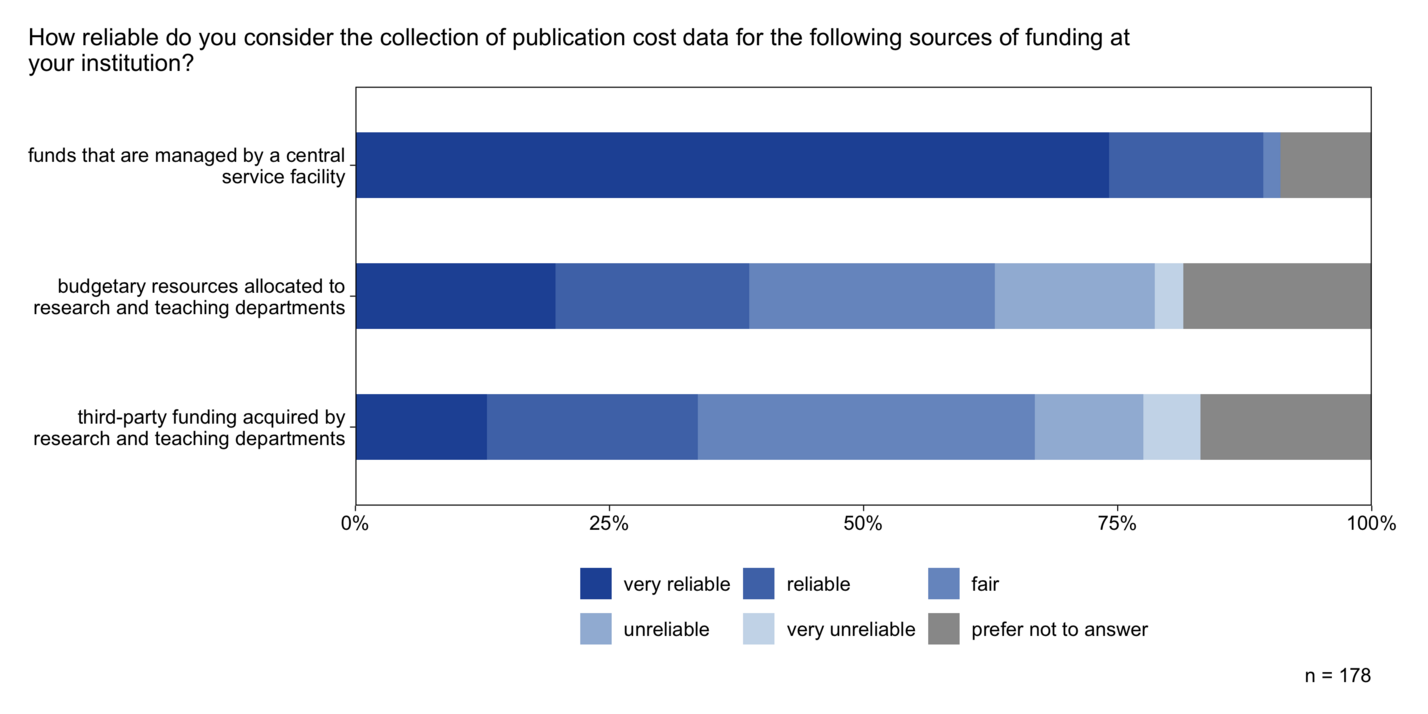

The subjective assessment of the reliability of the recording of publication costs varied by source of funding. The recording of third-party funded publication costs was considered the most challenging, whereas 89.3% of respondents considered the recording of publication costs covered by centrally administered funds to be “very reliable” or “reliable”. This assessment was shared by 38.8% of respondents with regard to publication costs covered by budgetary resources allocated to research and teaching departments and by only 26.4% of respondents with regard to publication costs covered by third-party funds acquired by research and teaching departments (see Figure 5).

Figure 5: Assessment of the reliability of the recording of publication costs covered by (a) funds managed by a central service facility, (b) third-party funds acquired by research and teaching departments, and (c) budgetary resources allocated to research and teaching departments.

Importance

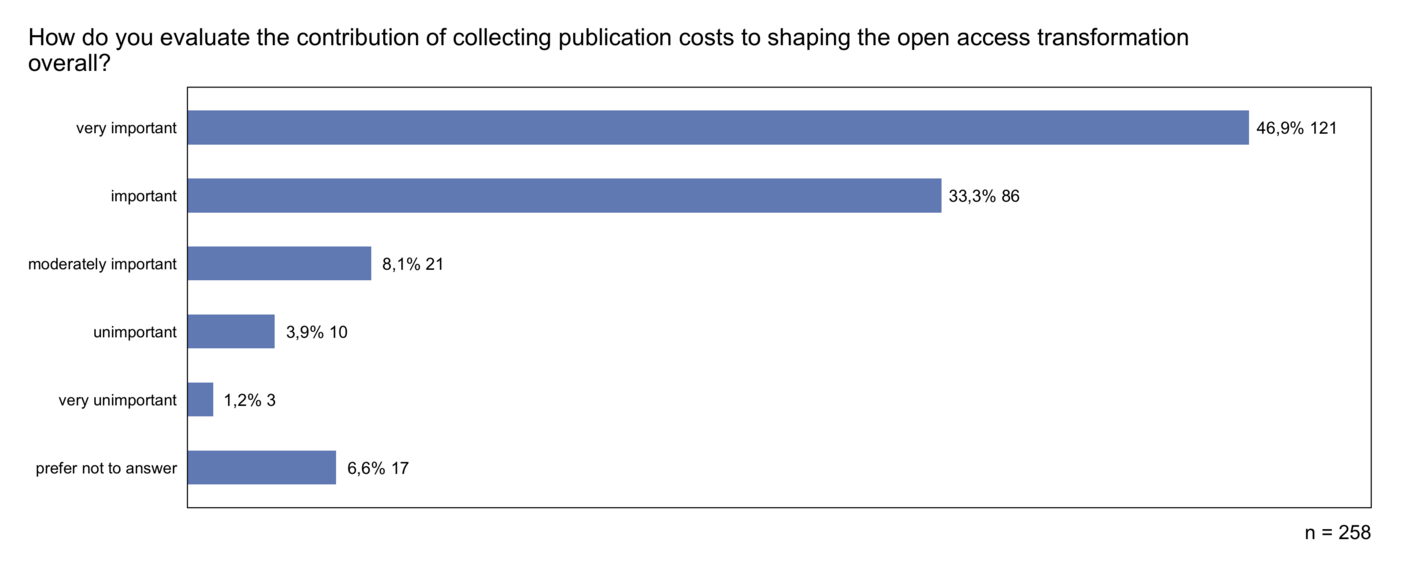

Some 59% of respondents stated that recorded publication costs were the basis for strategic decisions at their institutions. About a quarter of respondents stated that this was not the case. Eighty percent of respondents rated the contribution of the recording of publication costs to shaping the open access transformation as “very important” or “important” (see Figure 6).

Figure 6: Evaluation of the contribution of the recording of publication costs to shaping the open access transformation.

Conclusion

The survey shows that monitoring activities have not yet been established nationwide in Germany. Although some institutions already systematically record their publication output and publication costs, the data basis remains incomplete overall.

Many institutions that record publication costs have already established binding processes, while others are still in the process of establishing or defining workflows. The manner in which publication costs are recorded also varies – some institutions have already centralised the recording of these data, whereas at other institutions the costs are recorded on a decentralised basis and subsequently aggregated.

The evaluation of the quality of the recording of publication costs differed by the source of funding. The recording of publication costs covered by centrally managed funds such as publication funds was considered to be by far the most reliable. The central management of funds therefore contributes significantly to cost transparency. Institutions seeking to achieve reliable recording of funds, for example in the form of an information budget, can support this through the centralised management of publication funds. Publication funds financed from library resources (budgetary and third-party funding) have already proved their worth.

Although 80% of respondents considered the recording of publication costs to be important in the context of the open access transformation, these data were included in decision-making processes in only 59% of the institutions. This observation shows that the recording of publication costs has not yet had a broad impact on decision-making processes. This underscores the need for approaches to integrate cost data into decision-making processes. The study raises further questions for information and library science research, for example regarding (a) strategic options for action for research performing institutions as a result of the creation of cost transparency and (b) obstacles to the implementation of information budgets.

The survey results have been published in full. Anonymised survey data have been published via Zenodo (Strecker et al., 2025a). The results are described in detail in an article in the open access journal Bibliothek – Forschung und Praxis (Strecker et al., 2025b).

References

- German Science and Humanities Council (WR). (2022). Recommendations on the transformation of academic publishing: Towards open access. www.wissenschaftsrat.de/download/2022/9477-22_en.pdf

- Mittermaier, B. (2022). Das Informationsbudget — Konzept und Werkstattbericht. O-Bib. Das Offene Bibliotheksjournal, 9(4), 1–17. doi.org/10.5282/O-BIB/5864

- Pampel, H. (2019): Auf dem Weg zum Informationsbudget. Zur Notwendigkeit von Monitoringverfahren für wissenschaftliche Publikationen und deren Kosten [Working paper]. doi.org/10.2312/os.helmholtz.006

- Strecker, D., Pampel, H., & Höfting, J. (2025a). Dataset for: Recording of publication costs at research performing institutions in Germany (Version 1.0) [Dataset]. Zenodo. doi.org/10.5281/zenodo.14732554

- Strecker, D., Pampel, H., & Höfting, J. (2025b). Erfassung von Publikationskosten an wissenschaftlichen Einrichtungen in Deutschland. Bibliothek – Forschung und Praxis, 49(2). doi.org/10.1515/bfp-2025-0008

Suggested citation

Höfting, J., Pampel, H., & Strecker, D. (2025). Wie erfassen wissenschaftliche Einrichtungen Daten zu Publikationskosten? open-access.network. doi.org/10.64395/jm6zp-5cy42.

This article is licensed under the Creative Commons Attribution 4.0 International Licence (CC BY 4.0).